Exbo Group Q2 2025 EdTech Report

.jpg)

After a decade of volatility, the EdTech market is settling into disciplined, fundamentals-driven expansion.

.jpg)

The Maturing of EdTech: From Crisis Growth to Constructive Capital

After a decade of volatility, the EdTech market is settling into disciplined, fundamentals-driven expansion.

I. A Market Learning Discipline

By mid-2025, the U.S. education technology market had entered its most rational phase in more than a decade. The speculative energy of the pandemic boom had subsided, and the slew of take-privates in 2023–24 (when Bain’s $5.6 billion PowerSchool acquisition and Instructure’s recap dominated headlines) had cooled. In their place, investors and operators alike were returning to the fundamentals that define more mature software categories: durable customers, measurable impact, and disciplined capital allocation.

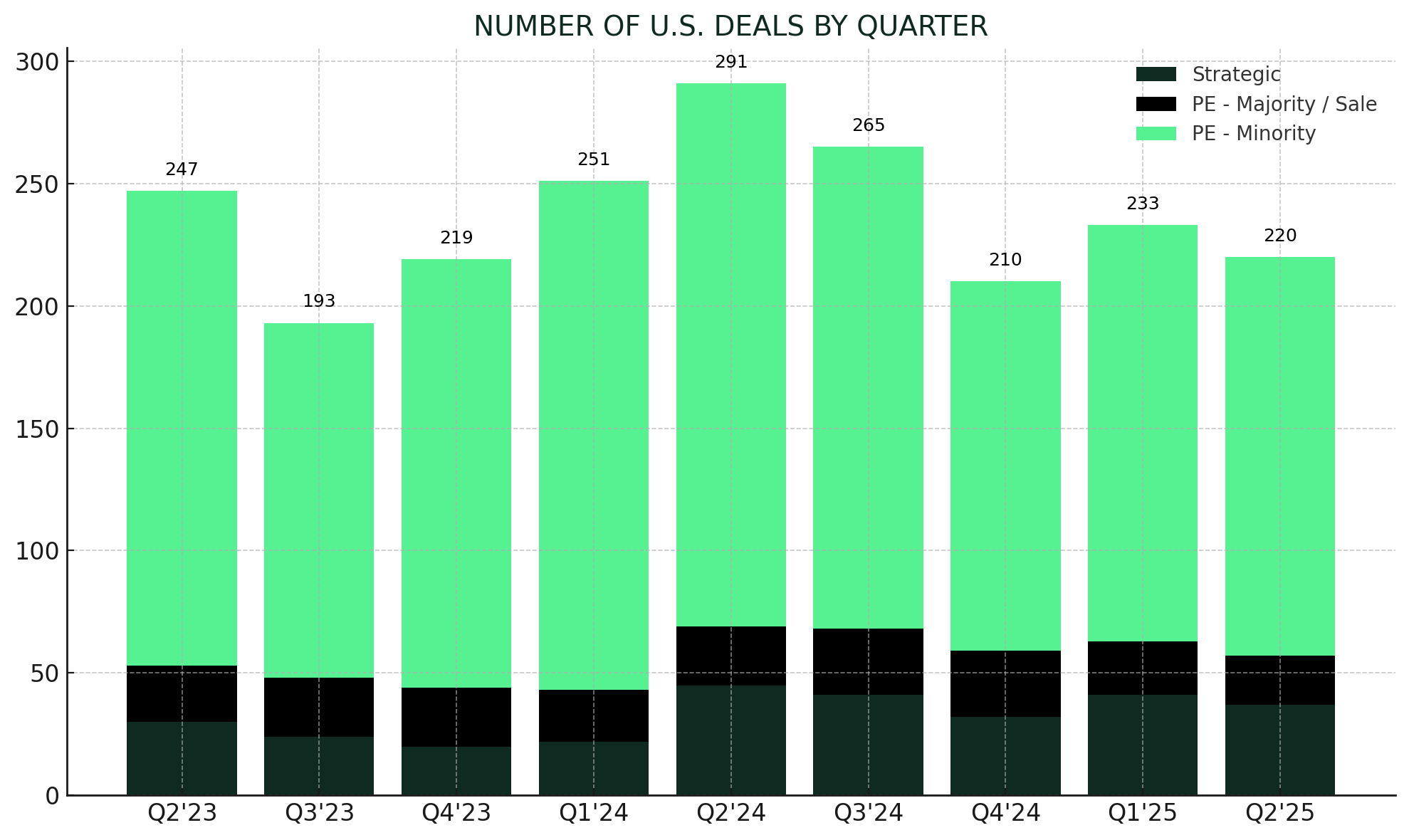

PitchBook data put the quarter in perspective. 220 U.S. EdTech transactions closed in Q2 2025, a modest 5.6 percent decline quarter-over-quarter and 24 percent year-over-year, well within the three-year range that now marks a normalized market.

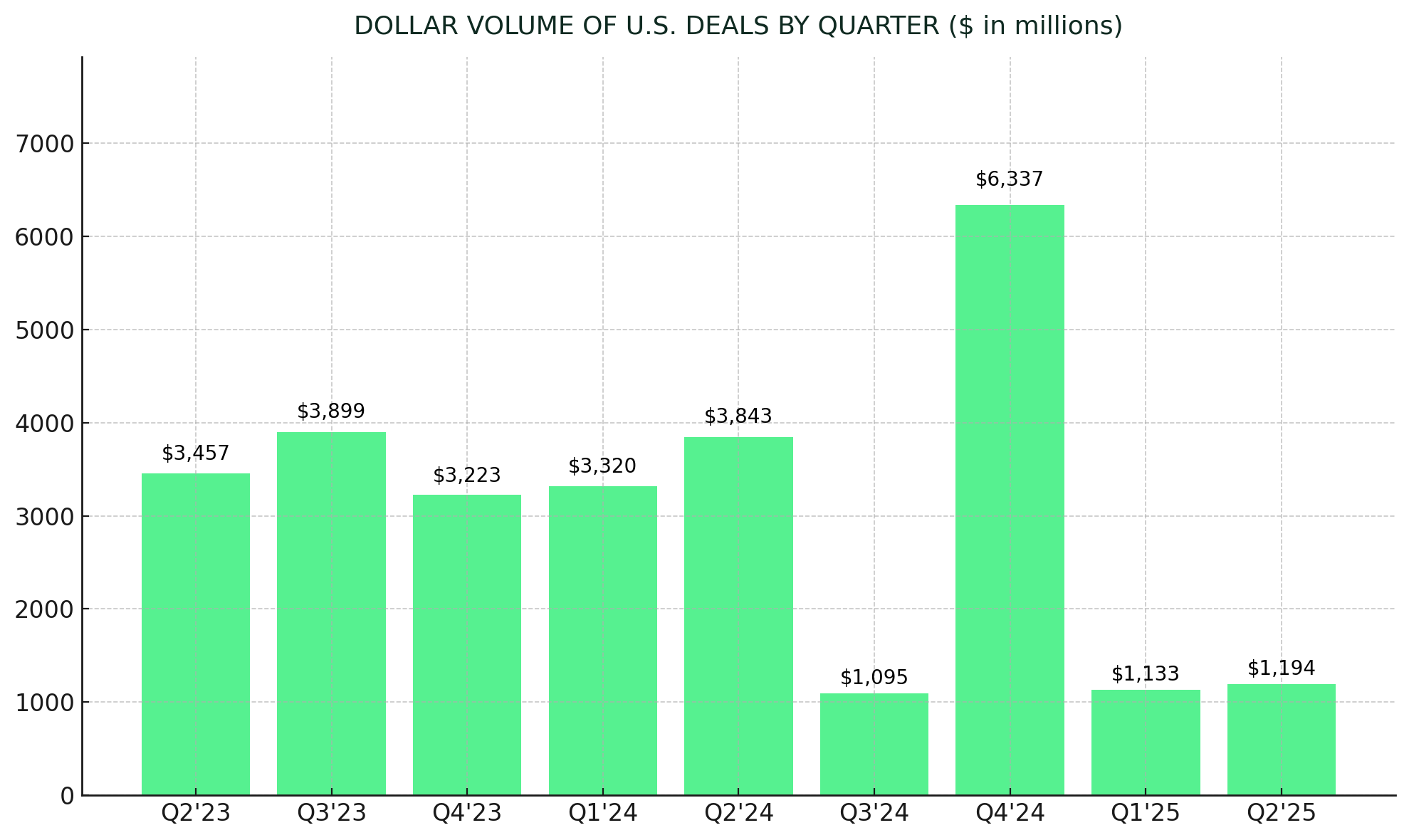

Disclosed deal value edged up to $1.19 billion, a 5 percent sequential lift from Q1’s $1.13 billion.

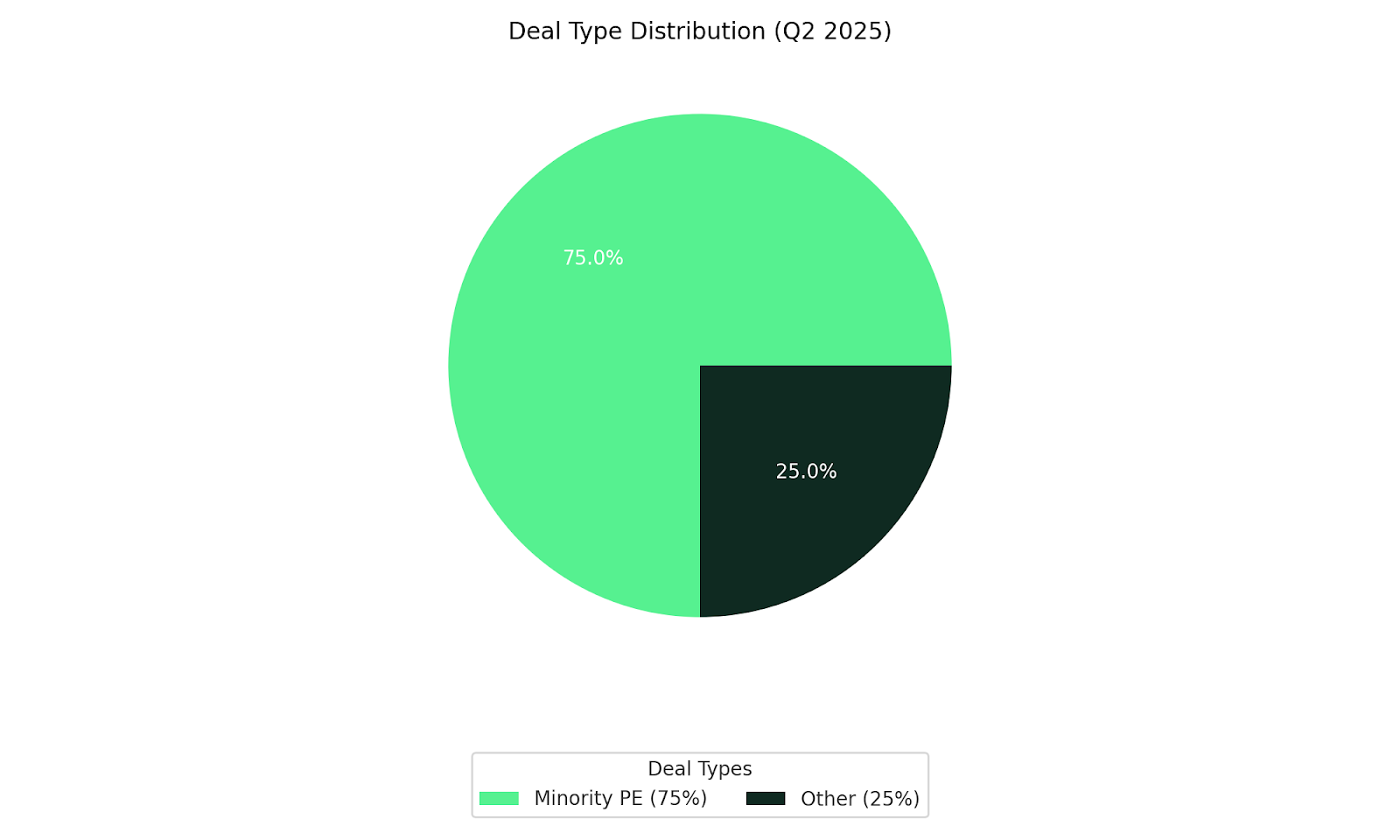

The real signal, however, was that roughly three-quarters of transactions were minority private-equity checks, representing 59 percent of total disclosed value. This is the hallmark of a market rediscovering growth through disciplined capital, rather than mega-rounds based on potential.

Three macro forces shaped the quarter’s mood. The first was the post-ESSER fiscal reset, as districts closed out pandemic-era stimulus and reverted to local funding cycles. The second was stabilization in higher education, where the Department of Education’s clear FAFSA calendar brought added predictability to admissions and financial aid cycles. The third, and arguably most significant, was the enduring strength of workforce learning, buoyed by new U.S. and European investment in apprenticeships and employer-driven upskilling. Together, these forces shifted EdTech from a “category of hope” to a “category of proof.”

II. The Macro Landscape: Fewer Headlines, Healthier Fundamentals

The broader education finance backdrop helped enforce discipline. The FY26 House Labor-HHS-Education appropriations bill proposed a 15 percent cut to the Department of Education, reducing total funding to $67 billion and slashing Title I by 27 percent ($5.2 billion). It also rescinded nearly $1 billion from FY25 Title I allocations. The bill clarified funding priorities: even amid overall reductions, Congress directed modest increases toward programs with consistent, measurable ROI: special education (IDEA, +$26M), charter schools (+$60M), and career-technical education (+$25M).

For investors, it underscores the broader shift of government dollars towards evidence-backed, outcomes-driven segments, particularly towards products that reduce operating risk or improve measurable outcomes.

The focus on operational efficiency and measurable outcomes will be critical within higher-education institutions as well, after a flat funding cycle for Pell Grants ($7,395 per student) and cuts to Federal Work-Study (-37 percent to $779 million).6

Fiscal tightening will prune the field, and policymakers have made clear what federal and state dollars will and won’t support. These forces are coalescing to re-anchor the market around a clear preference for demonstrable value over potential.

III. K–12: Pragmatism Over Proliferation

Nowhere is the return to fundamentals more visible than in K-12. After three years of inflated experimentation, districts have narrowed their focus to the platforms providing core services that keep schools running.

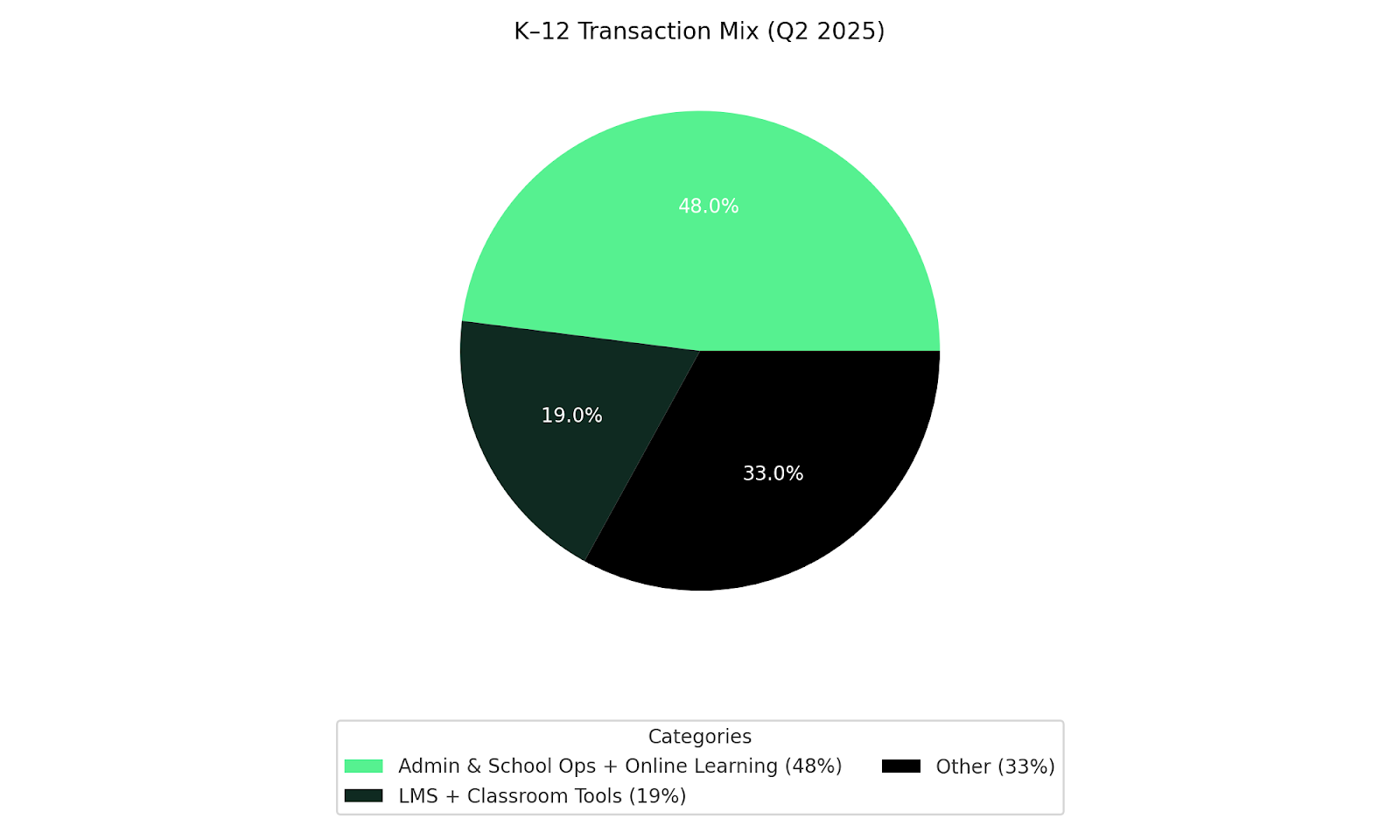

With ESSER III obligations closed and only narrow liquidation extensions available, administrators are prioritizing systems that safeguard compliance, accountability, and staff capacity. Administrative and School Operations tools, combined with Online Learning platforms, made up roughly 48 percent of Q2 transactions, while LMS and Classroom tools added another 19 percent. The pattern mirrors the behavior of superintendents, who are replacing complex stacks of apps with a shortlist of robust systems that handle student information, budgeting, attendance, and communications in one environment.

The fiscal posture of the states reinforced that discipline. By August 2025, nearly every state budget had been finalized for FY26. The aggregate signal was modest optimism, with a pragmatic approach. Arizona launched a $3.4 million “9th Grade Success” early-warning system. Colorado added $6 million to sustain universal preschool and $12.6 million for early-intervention services. Connecticut created a $300 million childcare fund and a $36 million early-childhood endowment. Montana passed the $100 million STARS Act to raise starting teacher pay and expand career-technical education. Nevada’s $12.9 billion K–12 budget incorporated equity-weighted, outcomes-based allocations plus $5,000 staffing bonuses. Texas combined an $8.5 billion school-funding package with a $1 billion ESA program offering $10,500 per student—and up to $30,000 for students with disabilities. West Virginia expanded its Hope Scholarship to universal eligibility and added a statewide digital-literacy push.

The deal market echoed that pragmatism. Strategic acquirers and financial sponsors targeted the ‘plumbing’—network and security infrastructure (Ednetics), digital-content delivery (Newsela’s $100 million acquisition of Generation Genius) , and financial-aid or enrollment workflows (Next Gen Web Solutions).

Without ESSER funding to chase, competitive advantage shifted toward documented efficacy and cost efficiency. Vendors that can quantify total cost of ownership and tie product use to measurable outcomes (particularly: attendance, reading proficiency, budget transparency) are retaining share. Public markets are rewarding the same profile. Stride traded around 2.8x 2025E revenue and 11.6x EBITDA. The broader education-technology cohort clustered near 3.2x and 14.7x, respectively., Today’s premium multiples come from cash-generative, renewal-driven operators.

Experts expect measured but resilient growth through 2026. Digital penetration in K-12 remains below five percent of total education spending. As the post-ESSER “prove-it” phase ends, multi-year renewals and selective platform consolidations should drive a slow but steady re-acceleration.

IV. Higher Education: Modernization Over Momentum

Higher education, by contrast, has traded existential risks for operational realism. The FAFSA meltdown of 2023-24, which derailed admissions and aid workflows nationwide, gave way to improved administrative stability.

The Department of Education’s August 2024 announcement of a revised rollout set the tone, establishing limited testing on October 1 and full FAFSA availability by December 1, 2024. Institutions could finally plan communications, packaging, and yield management around fixed dates. The agency’s further confirmation that the 2026–27 FAFSA will launch on schedule (October 1, 2025) cemented confidence.

The numbers validated this mood. Spring 2025 enrollment rose 3.2 percent year over year, with community colleges leading the recovery. That tailwind supported deal activity across enrollment, student success, and credentialing.

Within Q2 alone, buyers acquired RedShelf (digital content delivery), Enroly (international enrollment automation), and Next Gen Web Solutions (financial-aid and work-study infrastructure). The moves built on a string of earlier transactions: Ellucian’s acquisition of EduNav, Instructure’s purchase of Parchment, and Roper Technologies’ buyout of Transact. Each reflected the thesis of modernization through connecting academic planning, student records, and payments into a single operating core.

Policy risk remains present but bounded. A new federal order will require institutions to report admissions data disaggregated by race and sex, beginning with the 2025–26 cycle. At the state level, California extended accreditor recognition through 2029, enabling distance-education reciprocity through 2028.

Public markets show how investors are parsing the landscape. Duolingo continues to trade at a growth-premium multiple after record user and revenue performance. Docebo exceeded expectations on both top- and bottom-line results, expanding its AI-driven enterprise learning suite. The sector medians of (~3.2x 2025E revenue / 14.7x EBITDA for EdTech, ~2.1x / 9.3x for Education Services) set the reference points for mid-teens growers with consistent profitability.

Operationally, university leaders are now focusing less on new enrollment and more on retention, modality flexibility, and employer alignment.

The pandemic’s experiment with fully outsourced online-program managers (OPMs) has faded; modular, first-party credential stacks and skills-based pathways are taking their place. The most credible vendors are those with interoperable systems—records, advising, and analytics—and clear return-on-investment evidence.

The next twelve months will likely bring continued consolidation of advising, financial-aid, and career-services software, as institutions pursue integrated “student-success funnels.” The sector’s new reality: slow growth, but better data and cleaner execution.

V. The Future of Work: Education’s Secular Growth Engine

While K-12 and higher ed moved laterally, the future-of-work segment remained the engine of sector growth. It has held roughly 10 percent of total deal count, but its strategic relevance is disproportionate.

The story here is largely one of alignment: employers, educators, and governments are converging around an investment pattern focused on skills, credentials, and measurable job outcomes.

In June 2025, the U.S. Department of Labor awarded $84 million to expand Registered Apprenticeship capacity across states and territories. Across the Atlantic, the European Union’s Pact for Skills reported 6.1 million workers trained since 2020., Both signals tie public dollars directly to private-sector learning outcomes and validate the ROI case for education software that shortens time-to-competency.

Deal activity reflects this convergence. Sponsors and strategics acquired assets across apprenticeship management, professional training, and certification. Among them: Babington, Ascendient Learning, and, earlier in the cycle, Cornerstone’s acquisition of Talespin and D2L’s buy of H5P. The pattern is unmistakably one of bolt-ons that deepen domain capability and stack seamlessly into broader learning-management ecosystems.

Public-market leaders underscore the trend. Docebo delivered continued outperformance through multi-use-case enterprise deployments. Udemy maintained double-digit growth in revenue in its enterprise division. Each company’s success rests on two factors: measurable skill-lift and verified impact on hiring and retention. Investors have rewarded both with premium EV/Revenue and Rule-of-40 metrics relative to the broader SaaS cohort.

The next generation of winners will likely follow the “vertical EdTech” playbook popularized by Esteban Sosnik—industry-specific learning platforms built around domain accreditation, simulation, and assessment. Sectors such as healthcare, automotive, legal, and hospitality are already yielding credible early models. With AI compressing content creation costs and enhancing analytics, these verticalized platforms can now scale more capital-efficiently while preserving defensible moats through compliance know-how and credentialing authority.

The economics are compelling. Instead of competing for a broad TAM, these companies focus on maximizing retention, driving higher LTV/CAC ratios and measurable employer ROI. That structure has turned workforce learning into a preferred hunting ground for private-equity buyers building add-on roadmaps through 2026.

VI. Proof Over Promise: The New Investor Playbook

Across all segments, one rule now governs value creation: proof beats out promise.

Investors are prioritizing core infrastructure with a clear, evidence-backed role; software that reduces friction in the organization, automates compliance, or enables measurable learning productivity gains. The best assets share a common profile:

• Net-revenue retention above 110 percent.

• Implementation payback within 12 months.

• Documented efficacy, expressed either in improved student outcomes or enterprise productivity metrics.

The opportunity remains vast. HolonIQ projects global digital-education spend at roughly $404 billion by 2025, still only five percent of total education outlays. In the U.S., revenues are expected to climb from $187 billion in 2025 to $348 billion by 2030 (a 13.3 percent CAGR). Within this opportunity, infrastructure layers (identity, records, enrollment, attendance, payments) anchor the market’s defensive core. AI-assisted teacher, advisor, and administrator tools offer productivity leverage. And vertical skills platforms remain the highest-beta but most proven growth vector, capable of compounding through bolt-ons and regional replication.

Multiples continue to reward discipline. Public comps demonstrate that sticky, renewal-based revenue and measurable outcomes still command valuation premiums even amid subdued deal counts. This is the picture of a maturing, not slowing, sector.

VII. Outlook: The Quiet Compounding Era

As 2025 progresses, U.S. EdTech will remain a multi-speed market. K–12 will renew selectively and consolidate point solutions into integrated operations suites. Higher education will sustain modest enrollment gains and prioritize interoperability between aid, advising, and career-service systems. Corporate learning will continue to outperform, driven by employer investment in compliance, safety, frontline skills, and AI literacy.

Deal activity will stay within a tighter band (expect fewer than 250 transactions per quarter) but the quality of capital will improve. Minority growth checks will dominate through 2026, and control transactions will increasingly center on platform assets with clear adjacencies.

Digital penetration remains shallow, but sentiment has strengthened. The speculative phase of EdTech is over; the infrastructure phase has begun.

The companies that will define this era will look less like consumer startups and more like software utilities; mission-critical, quietly compounding, platform-building.

At a high level, EdTech is beginning to behave more like traditional SaaS. For investors, that makes the next decade less about discovery and more about disciplined construction; the transition from crisis growth to constructive capital.

References

EdTech Deals (community tracker). (2025, Feb. 19 update). Selected 2024–2025 acquisitions and take‑privates.

Federal Student Aid (ED). (2024, Aug. 7). 2025–26 FAFSA Processing Timeline Update.

Grand View Research. (2025). Education Technology Market Summary (Market report). (Base year 2024; forecast through 2030).

HolonIQ. (2021). Education Technology in 10 Charts.

HolonIQ. (2025). The 2025 Europe EdTech 200 aligned to the Global Learning Landscape.

Oppenheimer & Co. Inc. (2025, March). EdTech Sector – FY 2024 Market Update (Investor presentation).

Raymond James Investment Banking. (2025, Q2). Education Technology Insight: Market Update (Newsletter; PitchBook‑sourced deal counts/values).

National Conference of State Legislatures. (2024). State Actions on Education Savings Accounts.

National Student Clearinghouse Research Center. (2025, May 22). Spring enrollment rises (news release).

U.S. Department of Labor. (2025, June 30). DOL awards nearly $84M to expand Registered Apprenticeship.

U.S. Department of Education. (2024, January 9). Updated Technical FAQs for Liquidation Extensions (ESSER III).

Whiteboard Advisors. (2025, Aug. 8). College Admissions Oversight Expands | What’s Next for NAEP | CogAT to Publish Post‑Pandemic Norms.

Whiteboard Advisors. (2025, Aug. 15). K‑12 FY26 Budgets Signal Cautious Optimism | ED Moves to Restrict PSLF Eligibility. Whiteboard Advisors Notes

Whiteboard Advisors. (2025, Aug. 29). State Higher Ed Policy Round‑up | HSI Definition Faces Legal Scrutiny | FAFSA to Launch on Time. Whiteboard Advisors Notes

Whiteboard Advisors. (2025, Sept. 5). What’s in the House Appropriations Bill? Whiteboard Advisors Notes

.png)